Low grown tea, rubber enjoy profits

Ravi Ladduwahetty

A presentation titled: “ The

profitability and the productivity of Sri Lanka’s Plantations - Tea and

Rubber Sectors and implications for wage determination” was delivered by

Dr Ramani Gunatilleke at the Sri Lanka Tea Board auditorium last

Tuesday. This was during the news conference held by the Planters

Association that day.

Dr Gunatilleke is a Consultant to the

World Bank, ILO and ADB.

The context of the presentation was Sri Lanka’s share of the global

market in commodities steadily declining which is generally attributed

to high costs of production and low levels of productivity compared to

competitors.

The growing importance of smallholders in the production of green

leaf, especially in the low country, reflects the different cost

structures they face relative to the Regional Plantation Companies (RPCs).

The RPCs are challenged to be more competitive.

She said that the objectives of the study has been to inform the wage

negotiation process, initiate a stock-take to inform the process of

developing long-term strategies for the sector as a whole, by the

Regional Plantation Companies themselves.

Another objective of the study was to provide stakeholders, including

policy-makers, with a rigorous and independent assessment of the

profitability and sustainability of the RPC sector.

Costs of production

One of the burning issues was the high costs of production vis a vis

the low levels of productivity compared to competitors.

The growing importance of smallholders in the production of green

leaf, especially in the low country, reflects the different cost

structures that they face relative to the Regional Plantation Companies

(RPCs).

The RPCs are challenged to be more competitive and Sri Lanka’s share

of the global market in commodities has been steadily declining, has

also been a bone of contention.

Profitability

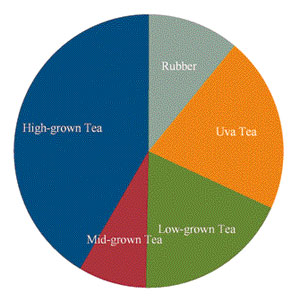

According to the study done by Dr Gunatilleke, only low grown tea and

rubber have been enjoying profits in the recent past. The high grown,

mid grown and Uva tea sectors have been posting losses, but the losses

have been stable rather than increasing over the years.

Impact of exchange rate movements on profitability was an important

issue which merits careful analysis which is beyond the scope of the

present paper, she said.

Productivity

She also noted that labour productivity had been stable in all the

sectors and so have yields other than in low grown tea where yields have

been declining.

Scatter plots of pooled real profits and productivity data of RPCs

for the fifteen years of the reference period, strongly suggest that

profitability is positively associated with labour productivity in all

five sectors.

The results suggest that increasing productivity is fundamental to

increasing profitability in the RPC sector.

Losses experienced by the high grown, mid-grown, and Uva sectors were

due to the sectors’ inability to increase productivity sufficiently to

offset high costs relative to those of competitors.

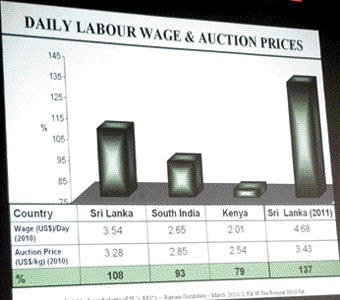

Costs

Results suggest that profitability of the low grown sector lie in the

processing of bought leaf rather than estate production as neither

labour productivity nor yields have increased. Tea is a labour-intensive

industry, so labour accounts for bulk of production costs.

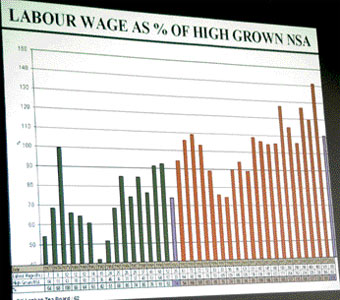

Labour costs including welfare amount to 46 percent of Nett Sale

Average in High Growns, 18 percent in Low Growns if total NSA was taken

into account but 31 percent if attributed NSA is taken into account

(difference due to the bought leaf component).

“With provisioning for gratuity, labour costs accounted for between

43 to 54 per cent of the NSA in the high grown, mid-grown, Uva and

rubber sectors in 2009,” she said.

Low grown has reported a much lower rate of 21 per cent because of

the bought leaf component. Long-term share of labour costs in NSA

appears relatively stable in all the sectors except rubber.

Management’s and materials’ shares of Net Sale Averages in the Mid

Grown sector have not been stable and materials costs in the Low Grown

sector have also not reverted to mean in the long-term

Graphical analysis of the share of compensation to labour in value

added: High Grown risen slightly, Mid Grown stable, Uva largely stable,

Low Grown declined, rose until 2001, declined until 2006, rose again

after that.

Productivity

Labour productivity has been stable in all the sectors and so have

yields other than in low grown tea where yields have been declining, she

said. Scatter plots of pooled real profits and productivity data of RPCs

for the fifteen years of the reference period, strongly suggest that

profitability is positively associated with labour productivity in all

five sectors.

The results suggest that increasing productivity is fundamental to

increasing profitability in the RPC sector. Losses experienced by the

high grown, mid-grown, and Uva sectors are due to the sectors’ inability

to increase productivity sufficiently to offset high costs relative to

those of competitors.

Results suggest that profitability of the low grown sector lies in

the processing of bought leaf rather than estate production as neither

labour productivity nor yields have increased.

Policy issues

Some of the policy issues, she said, range from:

*Should land productivity be increased through replanting, should

diversification into more productive activities, or both? Would

processing rather than green leaf production make more economic sense?

* How sustainable is the present system of a RPC sector-wide wage

determined through a model of centralized wage bargaining?

* Since there is such diversity in the sector, a one-size-fits-all

approach to wage bargaining appears not to be the most appropriate for

the sector.

* Uniform wage rate has only succeeded in moving workers out of the

industry as a whole, while making labour immobile within the industry

itself.

* Privatization of the management of the plantations appears not to

have entailed a sufficiently positive paradigm shift in the sector’s

orientation towards the market. |

")