|

CJ’S BLINKING ACCOUNTS:

OPEN AND SHUT CASE OF ACCOUNT FIXING/CORRUPTION

by S.P.C.

With the Parliamentary Select Committee hearings on the impeachment

of the Chief Justice due today, independent observers have expressed

shock and dismay over the manner in which some of her financial dealings

have been manipulated, with a view to hiding her true financial worth

from assessors.

Financial regulators for example would have been put off by the fact

that on repeated occasions over several years there was zero balance in

her accounts on significant dates such as March 1st or December 1st.

However, as soon as the dates passed, these accounts were replenished

with their regular millions. The initial study of the operations of Dr.

Shirani Bandaranayake’s account suggests a pattern of behaviour which

would easily arouse suspicion among any regulator, as the behaviour

displays many devious methods to avoid detection of the nature of the

transactions.

The operation also suggests that Dr. Bandaranayake has deliberately

and consistently acted in at least five consecutive instances to avoid

disclosure of the sums that were in her account and that the scheme has

been meticulously implemented in a highly sophisticated manner. A

further suspicion that may arise is as to whether Dr. Bandaranayake was

using her privileged position, first as a Supreme Court Judge and

thereafter as the Chief Justice, to indulge in this activity, knowing

fully well that her actions are very unlikely to be investigated by any

other regulatory agency. Being the Chief Justice of the country, does

not give such person immunity from the laws of the land. The law must

apply in a just and fair manner to all persons, however high and mighty

they may be.

Accordingly, it is now time for the law enforcement authorities to

commence a probe regarding the true nature of this Dr. Shirani

Bandaranayake’s highly suspicious financial dealings. If that is to be

done in an impartial manner, she cannot remain as the Chief Justice of

the country.

Justice must apply to the Chief Justice as well.

(a) the operation of several bank accounts by a person, which

suggests that multi-accounts are used to defuse the magnitude and

frequency of transactions in order to confuse regulators.

(b) the opening and closing of bank accounts within short periods of

time, which suggests that the accounts are used for a particular

transaction and then closed before suspicion is aroused in the minds of

the authorities.

(c) the manipulation of accounts to have low balances or zero

balances on certain significant dates, e.g. 31st December or 31st March,

(which are the dates that are generally used by regulators or

surveillance agencies to monitor accounts on a regular basis), in order

to reduce suspicion or evade detection by regulators.

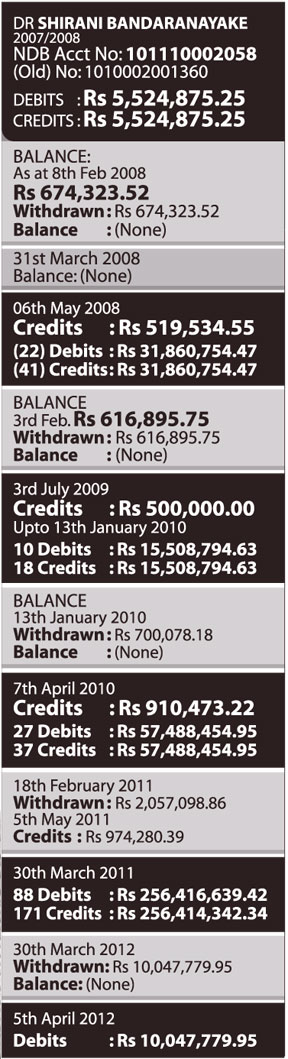

A careful assessment of Dr. Shirani Bandaranayake’s Account No.

101110002058 (Old No. 100002001360) maintained at the National

Development Bank (NDB) reveals the following:

(1) During the year 2007/2008, Dr. Bandaranayake maintains the above

account in an active manner, with four debits to the value of Rs.

5,524,875.25 and eight credits to the value of Rs. 5,524,875.25 being

transacted through the account. By 8th February 2008, a sum of Rs.

674,323.52 was lying to the credit of the account. On that date, the

entire amount is withdrawn, thus reducing the balance to zero.

Thereafter, no transactions took place and accordingly, on 31st March

2008, the balance in the account continued to remain at zero. On that

basis, Dr. Bandaranayake did not disclose the bank account in her Assets

and Liabilities Declaration, even though the rules pertaining to the

Declarations demand that a person discloses all accounts even if such

accounts do not contain any balances.

(2) The account lies dormant until 6th May 2008, on which date a sum

of Rs. 519,534.55 is credited to the account, and thereafter the account

becomes active, with 22 debits amounting to Rs. 31,860,754.47 and 41

credits amounting to Rs. 31,860,754.47 being reduced upto 3rd February

2009. Then, on 3rd February 2009, the entire sum of Rs. 616,895.75 which

was in the account on that date, is withdrawn and the balance is reduced

to zero. Thereafter, the account remains inactive, and on 31st March

2009, the account records a zero balance. Accordingly, Dr. Bandaranayake,

for the second time, does not disclose such account in her Assets and

Liabilities Declaration as at 31st March 2009.

(3) The zero balance remains until 3rd July 2009, at which point, a

sum of Rs. 500,000.00 is credited to the account.

Thereafter until 13th January 2010, the account is operated in a

highly active manner with 10 debits amounting to Rs. 15,508,794.63 and

18 credits amounting to Rs. 15,508,794.63 being recorded in the account.

However, on 13th January 2010, the entire sum of Rs. 700,078.18 lying

to the credit of the account is withdrawn, thus making the account

balance zero, once again. Such zero balance status in the account

remains as at 31st March 2010, and once again, for the third time in

succession, Dr. Bandaranayake does not disclose the account in her

Assets and Liabilities Declaration.

(4) The account lies inactive until 7th April 2010, and on that date

the account is credited once again with a sum of Rs.910,473.22 and the

account regains its usual robust character with 27 debits amounting to

Rs.57,488,454.95 and 37 credits amounting to Rs.57,488,454.95 being

recorded up to 18th February 2011. On 18th February 2011, the now

familiar total withdrawal occurs, and on that date the entire balance

lying in the account of Rs.2,057,098.86 is withdrawn, leaving the

account with a zero balance once again. Such zero balance is maintained

as at 31st March 2011, and yet again, for the fourth time in succession,

Dr. Bandaranayake does not disclose the account in her Assets and

Liabilities Declaration.

(5) The account remains inactive until 5th May 2011 in keeping with

the regular pattern that has by now been established, and on that date a

sum of Rs.974,280.39 is credited to the account and the account becomes

highly active once again.

This advanced level of activity continues until 30th March 2012, by

which time, 88 debits amounting to a staggering Rs.256,416,639.42, and

171 credits to a similar value of Rs.256,414,342.34 passes through the

account. But, as is now very familiar, on 30th March 2012 the entirety

of the Rs.10,047,779.95 that is lying to the credit in that account is

once again withdrawn in the established pattern, and the account is

reduced to zero once again. Such zero balance is recorded as at 31st

March 2012, and again, for the fifth consecutive time, Dr. Bandaranayake

does not disclose the account in her Assets and Liabilities Declaration.

(6) True to the pattern, a sum of Rs.10,047,779.95 is brought back to

the account on 5th April 2012, and the account resumes its active

character yet again.

It is obvious that, the methodology adopted in the operation of the

above account is a well thought out and sophisticated operation. It is

not an operation of an account that would be expected from any ordinary

person, let alone the country’s chief judge of the Supreme Court. The

magnitude of the figures and the careful avoidance of significant dates

is consistent with an intention to conceal the operation of the account,

and avoid detection. |

")