|

|

| Monday, 25 November 2002 |

|

|

| Business |

| News Business Features Editorial Security Politics World Letters Sports Obituaries

|

2002 set to be record year for Caltex Lubricants (Lanka) By Saruchi Dissanayake

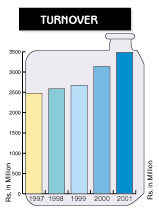

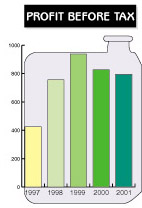

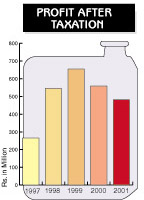

Caltex Lubricants Lanka Limited is one of the premier blue chip companies in Sri Lanka - the company's main line of business is in blending, importing, distributing and marketing lubricating oils and greases. Lanka Lubricants was originally the lubricating oil blending plant of Ceylon Petroleum Corporation and it was incorporated as a government owned company in December 1992. The company was privatised in 1994 with Caltex purchasing a 51% stake in the company. Caltex was an original player in Sri Lanka's petroleum industry - setting up operations here in the 1930s before having to exit because of nationalisation. The privatisation of Lanka Lubricants was the first major privatisation initiated by the previous UNP government in 1993 and the acquisition brought with it a number of concessions for Caltex. Caltex Lubricants Lanka Ltd. was listed on the Colombo Stock Exchange in 1996. The parent companies of Caltex - Chevron Corporation and Texaco Inc. merged late last year - to create the fifth largest energy firm globally and the fourth largest publicly traded energy company in the world. Chevron Texaco ranks third in the world's oil reserves and fourth in oil and natural gas production. It has world class upstream position in reserves, production and exploration opportunities as well as a worldwide refining and marketing business and a global chemicals business. ChevronTexaco has a refining capacity of 2.2 million barrels per day. The company has operations in more than 180 countries and employs over 50,000 worldwide. Caltex is the market leader with 97% of market share, and according to Avancka Herat, Manager - New Business Development at Caltex Ceylon Ltd, the strength and performance of the company is reflected in its share price. He pointed out that the dividend yield was close to 14% last year and with the share price appreciating, the current dividend yield is about 9%. Herat said the company was in a strong cash position with around two billion rupees cash at present. Cash flow per share is about Rs. 60 with the share trading at Rs. 115 on 07.11.2002. The Caltex mandate in Sri Lanka so far has been investing in lubricants only but Herat said that with the opening of the Petroleum industry, the cash would be used for expansion. Herat said 2002 is set to be a record year for the company, adding that a significant recovery has already been made in terms of growth after a difficult year last year. Caltex is targeting growth of around 9% this year, and 8-9% next year. The company's commercial market too has shown high growth this year especially with significant power capacities added on after last year's power crisis. In particular, he identifies the North and East as an area with the biggest growth prospects. The company expects to see up to 100,000 new motor vehicles in the area which will increase their market base. As far as the challenges faced by the company go, Herat identifies as the biggest challenge, the liberalisation of the petroleum industry. The company's monopoly on local manufacture and distribution of lubricants through Ceypetco owned and managed service stations however will continue till 2004. However, according to Herat. the company has no immediate plans for expansion - he said. The plant was currently running at only 50% of capacity and therefore can double production merely by running two shifts. He said however that changes will be made to the distribution model and channel strategy with the opening of the petroleum market. He said Caltex had a product range to compete with any other brand - local or international as well as the technical knowledge, lab facilities and customer care. He said the management has excellent labour relations and hasn't had a single work day lost despite the plant being within the CPC compound. Jayantha Perera, Head of Research at DFCC stockbrokers recommends Caltex stock as a good buy because it has the strength of being a multinational while also enjoying high cash flow and high earnings growth. He said the stock should also be attractive to foreign buyers because of the international image of the parent company Chevron Texaco. Perera said that the company's inventory has come down against last year showing more operational efficiency and higher turnover levels, while the capital requirement has also been lowered which in turn reduces interest costs. With the budget proposal to reduce corporate tax by 5%, Perera expects Caltex, which has a big tax component, to enjoy savings of around Rs. 20-30 million. He expects the company to record 28-30% growth in after tax profits this year. Perera said that Caltex is a net finance income earner - the company's financial income is higher than its financial costs. He expects financial income to move down slightly with interest rates coming down, but said the shift would not be considerable. He said the company's liquidity position is its biggest strength as it can move into other financial sectors and try to consolidate itself. The strong cash position means the company can engage in horizontal or vertical integration. He said the high liquidity can also make it difficult for new entrants to compete against Caltex. He expects however that new entrants such as Shell and BP would be able to mount strong competition. In the last financial year ending December 31, 2001, the company's profit before tax was down 3.8% at Rs. 796.3 Million compared with Rs. 827.9 million in 2000. After tax profit was down 13.83% at Rs. 481.7 million. The year was described by Managing Director Kishu Gomes as the most challenging year faced by Caltex since its return to Sri Lanka in 1994. Gomes noted that broader economic pressure such as the September 11 attacks, the US economic slowdown and the weaker rupee took a toll on the company's volumes. Operating expenditure rose nearly 33% year on year - mainly because of a one off provision of Rs. 73 million for a Voluntary Retirement Scheme. Net turnover was 11.2% higher at Rs. 3.5 billion - due largely to higher prices. In the last financial year, the Managing Director called for a tough decision to face the tough times and launched a cost restructuring program that included plant restructuring, the offer of a Voluntary Retirement Scheme for excess staff, and a re-assignment of responsibilities of employees. The restructuring initiatives were expected to result in an annual saving of almost Rs. 50 million this year. The lubricants market witnessed an 8% decline in volumes in 2001 because of weaker consumer demand, longer oil drain intervals and a slowdown in motor vehicle population growth broadly in line with the slowdown in GDP growth and consumer demand in other sectors and product. Caltex noted that the power crisis led to the closure of many small to medium scale industries but lubrication was still a need for the generation of thermal based power. In the three months to September 30, net profit after tax was Rs. 288 million - 167% higher than the Rs. 108 million recorded in the same period last year. Profit before tax was 102% higher at Rs. 411 million comparedto Rs. 204 million in the 3rd quarter of 2001, while Operating Profit was Rs. 359 million - 115% higher than the Rs. 167 million recorded in the same period last year. Gross Profit was in the third quarter this year amounted to Rs. 439 Million - 43% higher than the 307 million recorded last Caltex recorded Rs. 1, 026 million of sales in the three months to September 30 - a 17% increase over Rs. 878 million recorded last year. Chairman Martin B. Southern said overall sales volume grew by 9% benefiting from increased sales in the North and East, Power Generation sector and 2% growth in export volumes. He said the removal of the income tax surcharge and the stability of the local currency towards the latter part of this year helped the company maintain the current price level. Southern said in a statement to shareholders, that the re-structuring program and other cost reduction initiatives undertaken by Caltex Lubricants Lanka Ltd, have so far realised a saving of over Rs. 40 million. He said the company was reaping the benefits of the ChevronTexaco merger as it has rebates on core raw materials such as base oil and additives through global supplier agreements. The chairman said that these benefits coupled with the merger related service charge rebates have so far contributed approximately Rs. 100 million. |

|

News | Business | Features

| Editorial | Security

Produced by Lake House |