|

First half performance in licensed commercial banks:

Drop in lending rates affects income

Prasad Polwatte and Asanka Liyanage

Domestic financial markets were somewhat volatile at the beginning of

2009. It became more liquid and stable in the second half of 2009 and

first half of 2010 with the declining inflationary pressures and the

easing of monetary policy, resumption of capital inflows due to reduced

risk aversion and improved investor sentiment following the end of the

hostilities. stronger capital positions and enhanced risk management

infrastructures that had been instituted have placed the financial

sector on a stronger footing to absorb the impact of the economic

slowdown.

Financial markets were more stable with improved liquidity and

declines in interest rates from the beginning of 2010.

The exchange rates were more stable. Equity prices have surged

upwards during the year. The banking sector sustained its earnings via

an increase in investment income from government securities and

equities.

Almost all banks have adopted investing funds in long term

investments rather than in short term investments. On the other hand

they encourage short term borrowings as it was less costly than the long

term borrowings.

In this article an effort has been made to compare and contrast the

performance of Licensed Commercial Banks (LCBs) first half 2009 and

2010. Both public and private LCBs overall performance was comparatively

higher in first half of 2010 compared to the 2009. All of the key

performance indicators showed positive signs averagely within the

sector.

Summary of Key Performance Indicators of first Half of 2010 and 2009

of Leading LCBs is presented in table 1.

Table 1: Summary of Key Performance Indicators

Name of Profit for Total Assets Market price Return on Return on

the Bank the period Rs Mn at half end shareholders’ Assets

Rs Mn Rs funds% before tax %

2010 2009 2010 2009 2010 2009 2010 2009 2010 2009

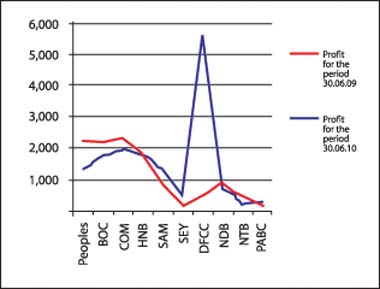

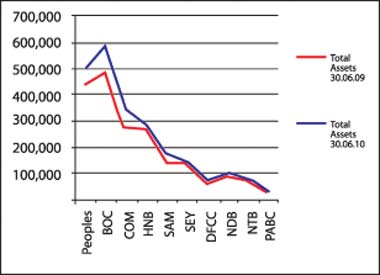

Peoples 2,178 1,310 500,901 442,640 N/T N/T 23.40 15.90 1.70 1.20

BOC 2,195 1,793 587,026 493,829 N/T N/T 17.62 15.08 1.28 1.11

COM 2,314 1,977 337,943 273,517 178.50 134.00 15.98 15.11 2.46 2.35

HNB 1,792 1,773 286,240 266,971 282.00 120.00 14.96 16.84 2.05 2.07

SAM 1,302 830 170,253 143,405 359.25 109.00 21.18 16.62 2.19 2.19

SEY 511 138 140,946 137,951 81.75 35.00 9.41 3.89 1.18 0.19

DFCC 6,031 661 61,574 56,171 267.75 135.25 37.10 12.90 12.10 4.30

NDB 699 896 94,938 86,888 245.00 153.00 11.51 13.35 1.33 1.60

NTB 444 211 78,058 77,295 55.50 30.50 17.58 10.96 2.28 2.10

PABC 151 299 23,909 20,122 32.00 13.75 13.76 34.21 1.34 3.06

Source: Published Interim Financial Statements of respective banks |

An overall drop apart from DFCC bank can be seen in total revenue

compared to 2009 first half in 2010. The main reason was drop in

interest income by averagely 15 percent in 2010 first half compared to

2009.

In the case of DFCC bank the results of 2010 included profit relating

to the sale and change of classification of part of the Bank's

shareholding in Commercial Bank of Ceylon PLC (CBC).

Table - 2 Average Weighted Prime Lending Rates (AWPLR)

As at Date Weekly Monthly Six Month

30-06-2010 10.37 10.47 10.68

30-06-2009 15.54 16.20 18.38

Source. http://www.cbsl.gov.lk |

Table - 3 Treasury Bills Interest Rates

As at Date 91 days 182 days 364 days

30-06-2010 8.07 8.93 12.34

30-06-2009 11.41 12.03 12.34

Source. http://www.cbsl.gov.lk |

The contribution to profit after tax from the transactions related to

CBC was Rs 5,282 million for the Bank.

The main reason for the drop in interest income was drop in lending

rates from 15 percent- 18 percent to 10.3 percent- 10.6 percent range in

2010 (Source. http://www.cbsl.gov.lk/). Even though an increasing trend

was visible in the growth in Advance portfolio of the banks

(Approximately 5 percent -10 percent) but the interest income had

dropped mainly due to the decrease in Average Weighted Prime Lending

Rates (AWPLR).

On the other hand LCBs concentrated on Government securities

specially Treasury bills, of which interest rates were decreased by

considerable percentage. Details are as follows.

Table 2

A material decrease in interest expense was shown in first half of

2010 to 2009. (Averagely 25 percent to 40 percent drop in all banks).

The decrease in the Average Weighted Deposit Rates (AWDR) was the main

factor for this interest cost reduction. It is clearly evident in the

following table.

Table 4

Table - 4 Average Weighted Deposit Rates (AWDR)

Date Monthly 6 month Fixed Deposit

Rate Rate Rate

30-06-2010 7.00 7.26 9.40

30-06-2009 11.12 11.48 15.26

Source. http://www.cbsl.gov.lk |

The deposit growth in 2010 first half has not proportionately

increased the interest cost in LCBs due to the drop in AWDR. On the

other hand banks were unable to attract more deposits since short term

deposit interest rates were less attractive and customers tend to switch

for more attractive investment opportunities in Capital/Money markets.

Apart from NDB and PABC all other banks have recorded an increase in

their profit after tax in first half of 2010 compared to 2009. The same

increase can also be notified in Net asset per share, ROE and ROA.

Both Public and Private LCBs overall performance was improved in

first half of 2010 compared to 2009. All of the key performance

indicators showed positive signs averagely within the sector.

Table - 5 Market Prices and Book Price per Share

Date COM HNB SAM SEY DFCC NDB NTB PABC

30.06.2010 178.50 282.00 359.25 81.75 267.75 245.00 55.50 32.00

Market price

30.06.2010 134.00 120.00 109.00 35.00 135.25 153.00 30.50 13.75

Market price

30.06.2010 79.41 103.97 167.3 43.48 155.43 135.90 26.63 17.44

Book Value

Over/(Under) 99.09 178.03 191.95 38.27 112.32 109.10 28.87 14.56

value

Variance in 33.21 135.00 229.59 133.57 97.97 60.13 81.97 132.73

prices

Source http://www.cse.lk |

Two line charts

Share prices of all banks had been grown rapidly in 2010 compared to

the same half in last year. A substantial increase could be seen in all

banking sector companies.

It is clearly evident in the following table. (Please note in the

case of Commercial bank price mentioned at 30.06.2010 is after 1:2 share

split)

The banking sector is continuously seeking opportunities at North and

East for their market exposures. On the other hand the CBSL is of the

view that further decrease of interest rates in future is possible and

the banking sector should take in to account the amount of customer

deposits that can be overlooked due to further decrease in the interest

rates.

LCBS will face great challenges in the second half to sustain its

level of performance of the first half 2010. |

")